Bekaert – elevated quality at 8.2x P/E

(BEKB.BR, $2.5bn market cap, $1.5m ADVT, 61% free float)

Bekaert is a world leader in converting steel into all kinds of wire, cord and rope products.

This is a less acutely horrible business than it sounds. Compared to primary steelmakers, Bekaert is not as capital-intensive, and is far less beholden to commodity price cycles.

Instead, for decades Bekaert suffered from the typical chronic ailments of many family-controlled European industrial firms. High costs, low margins, lack of growth and weak capital allocation made for an unappetising investment proposition.

Radical change came in 2019. Baron Bert De Graeve handed over the chairmanship to outsider Jürgen Tinggren, former CEO of Swiss elevator giant Schindler. Tinggren quickly changed the entire executive team, bringing in a former Schindler colleague as COO and then CEO.

The new team cut costs, set clear new priorities, and delivered much better margins and free cash flow, plus a credible platform for future growth. Bekaert’s balance sheet is stronger now than any time this century. Yet the stock remains dirt cheap.

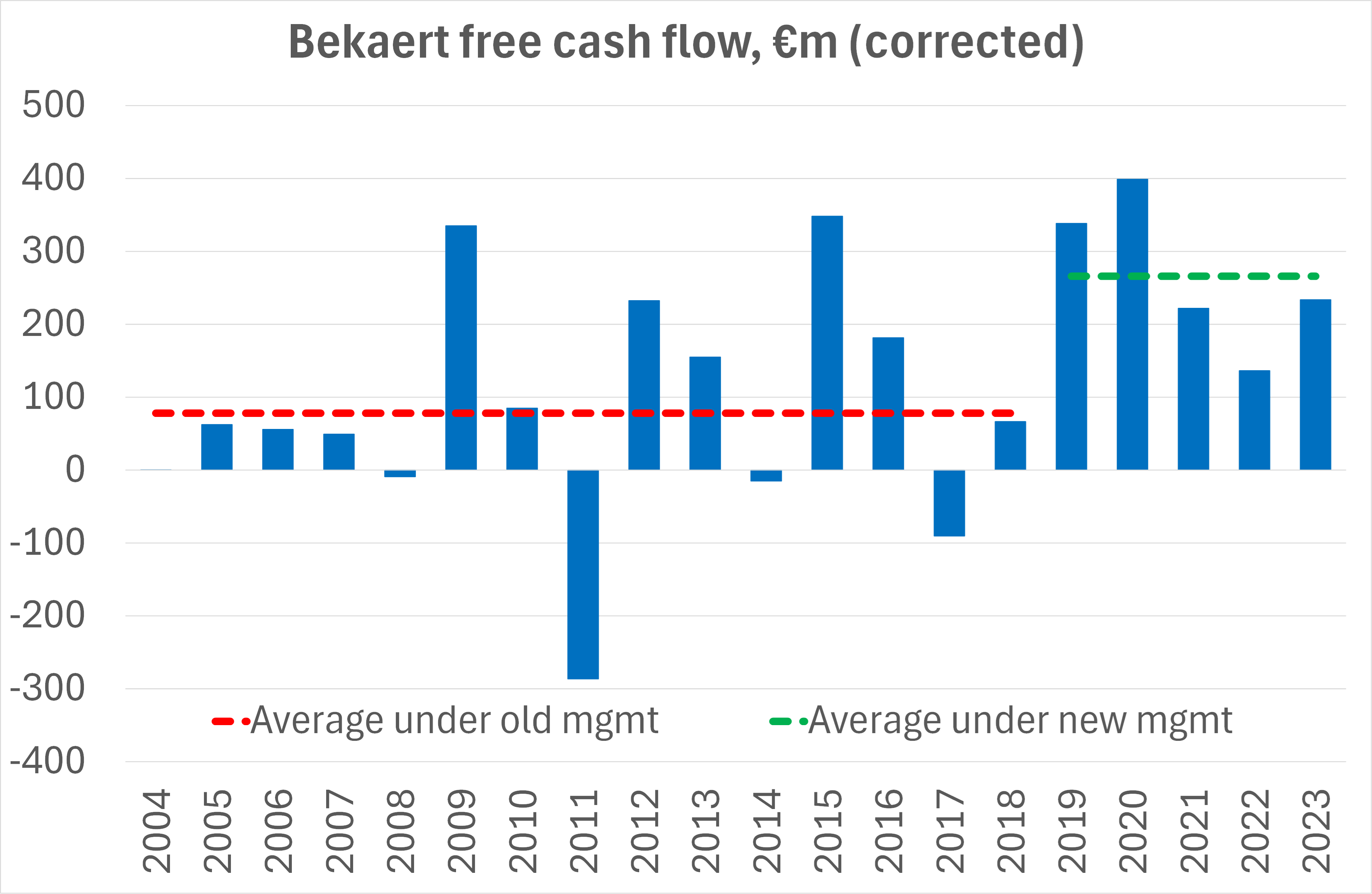

My chart below shows Bekaert has delivered €1.33bn of free cash flow in the last five years under new management. [NB this was corrected at 10:30am on 27/05/2024. The initial draft of the post gave a wrong figure of €1.5bn, having failed to correct for lease payments in the footnotes to the financing section of the cash flow statement. Many thanks to @GPK992 on Twitter for the spot.]

On a conservative estimate for 2024E, the stock trades on an 8.5% FCF yield, rising to 10.4%. It has returned more than €400m to shareholders via buybacks and dividends in the last two years alone.

This seems to me far too cheap, given the company’s strong balance sheet, improving margins and the profitable growth drivers from Dramix concrete reinforcement fibres, Currento hydrogen electrolyser components, and floating wind turbine anchor cables.

I have therefore started a position in Bekaert, which I intend to build over the coming months.

The post is organised as follows.

· Intro to Bekaert and details of its businesses

· History, management and ownership structure

· Financial review: is Bekaert high enough quality for a long-term holding?

· Estimates and thoughts on valuation

What is Bekaert?

Based in Belgium, Bekaert is a large global wire products company. It has 20,000 employees and 69 factories in 23 countries. In 2023 Bekaert processed 2.5 million tonnes of wire rod.

The end-markets served are undoubtedly cyclical: 47% mobility (mainly car and truck tyres), 17% construction and infrastructure, 10% energy and utilities, and the balance in agriculture, consumer goods, mining and various others.

By region, and including the profitable Brazilian JV, Bekaert’s 2023 sales mix was 36% EMEA, 29% Asia Pacific (of which 17% China), 19% North America and 16% Latin America.

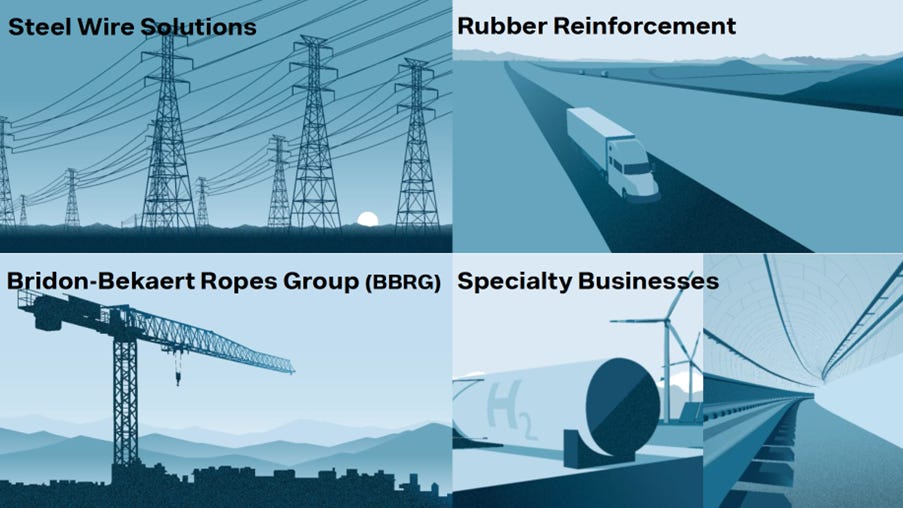

Bekaert has four segments which range from mature to growing. The new management team has lifted the profit contribution from the growth segments to 40% of total – see my chart below.

Bekaert’s organic growth target is 5% at group level in the medium term. This includes faster growers like Dramix concrete reinforcement fibres, Currento hydrogen electrolyser components, and floating wind turbine anchor cables. Meanwhile, tyre cord and other mature products will grow much slower than 5%, but with close attention paid to margins and free cash flow.

Full details on each segment follow.

Rubber Reinforcement (43% of sales, 40% of EBIT)

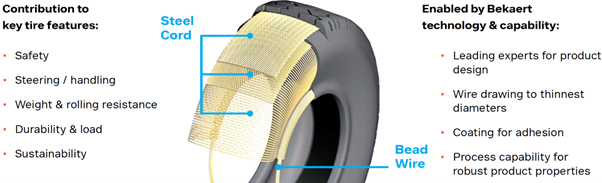

Tyre cord and bead wire remains Bekaert’s biggest business, though now down to only 40% of total operating profit in 2023, compared to 70% in 2018.

The graphic below explains the products.

Bekaert is the dominant global #1 player with c.30% market share. All the major tyremakers of the world are customers, and they rely on Bekaert to be a stable supplier. In the past Bekaert has acquired tyre cord plants from Bridgestone and Pirelli – tyremakers no longer want to make cord themselves. In my view, Bekaert’s relationship with its customers is as partners rather than adversaries.

Bekaert’s network of factories on every continent make it a local-for-local partner, unlike its Chinese and Korean rivals who rely on an export model. This could prove to be an advantage for Bekaert in future, if deglobalisation and trade wars pick up.

On the other hand, Bekaert is also deeply present in China, where it is so long established that it is regarded as a Chinese company. This acts as a hedge, because if Chinese tyremakers do enjoy great export success then Bekaert can benefit by supplying them in China.

Bekaert has a balanced 50:50 exposure to passenger cars and truck / bus, given that truck tyres use 10x more cord than passenger car tyres.

Replacement demand is far more important than OEM demand (tyres on new vehicles). As such, global miles driven is the key demand driver. This means Bekaert, like tyremakers in general, has lower cyclical exposure than carmakers in the event of a major recession. Bekaert sailed through the great financial crisis unscathed, for example.

Perhaps surprisingly, there is some scope for differentiation, competitive edge and growth within tyre cord. Lighter, stronger tensile cords contribute to overall light-weighting of cars and improved rolling resistance. These products reached 50% of total mix in 2023. Electric vehicles, with their heavy battery packs, require the strongest tyres and have been choosing Bekaert’s top-of-range Ultra Tensile cords.

Bekaert is vertically integrated, with its own engineering department and its own machines for wire-drawing and cord-making.

Under new management, Bekaert is realistic that tyre cord will not be a growth business. It is being managed for margin and cash. Concrete examples include the closure of unprofitable plants in Figline, Italy in 2018 and in Chongqing in Q3’23.

The competitive landscape is somewhat consolidated, which is potentially favourable for discipline. In China the players behind Bekaert are Xingda (1899.HK, $371m), Shandong Daye (603278.SS, $385m) and Shougang Century (103.HK, $63m, Bekaert owns 12.5%).

Koreans Hyosung Advanced Materials (298050.KS, $1.2bn) and Kiswire (002240.KS, $407m) are also sizeable players. Hyosung AM reported W1,806bn of total Tire Cord revenue in 2023, including both PET and steel cord – only the latter is competitive with Bekaert. Hyosung’s 2023 revenue is unchanged from 2017.

Steel Wire Solutions (27% of sales, 20% of EBIT)

SWS supplies diverse wire products across multiple sectors. The image below shows six examples. (Champagne cork wire and springs for insulin injection pens are sadly tiny niche markets, compared to the mainstay energy, construction and agriculture exposures.)

The new management team have made big improvements to SWS. Both margin improvement actions and disposals have played their role.

SWS’s EBIT margin has already doubled from 3-4% in 2018-19 to c.7% today. Bekaert targets a further 200bp improvement to 9% by 2026E. This is to be delivered by price-mix improvement and further portfolio optimisation. It’s a classic up-or-out approach which should be deliverable.

Bekaert already disposed of its large, low-margin Chile and Peru SWS businesses in 2023 for $136m. This disposal reduced Bekaert’s overall exposure to the volatile LatAm region, which had previously been overweight, considering also the large and profitable Brazil JVs.

In December 2023 Bekaert also decided to close two SWS plants in Indonesia and India.

Specialty Businesses (16% of sales, 24% of EBIT)

Dramix is the biggest and most important business in the Specialty segment. The product is specially shaped large staples (steel fibres) that are mixed into liquid concrete just before pouring, to provide a full reinforcing effect. This removes the need for labour-intensive traditional steel mesh or rebar, speeding up construction and reducing costs.

Bekaert invented Dramix way back in 1973. Concrete flooring and tunneling / mining are the most common applications, with around 20% global penetration.

Meanwhile, Bekaert’s latest-generation Dramix 4D and 5D products can also be used for demanding civil engineering and infrastructure applications, with just 1% penetration as yet.

Dramix has grown from €239m sales in 2018 to €335m in 2023, with much higher profitability. It is the key reason that the overall Specialty segment margin has reached 17%, a key factor in Bekaert’s groupwide margin improvement.

Bekaert is the global #1 player in the SFRC category (steel fibre reinforced concrete) with 40% share. Bekaert is three times as big as the second player. There’s a long penetration runway ahead, as conservative construction users and specifiers gradually learn of the benefits over traditional reinforcement. Europe has been the early adopter of SFRC (especially Germany and Poland), and Bekaert’s sales in Americas and Asias are now catching up.

Currento for hydrogen electrolysis is the other supposed exciting growth business within Specialty. Specifically, Bekaert supplies Currento-branded titanium porous transport layers (PTL) for proton exchange membrane (PEM) electrolyser manufacturers. PTLs account for 15% the PEM stack value, and Bekaert is the leader, supplying most of the top 10 OEMs.

Currento revenue doubled in both 2022 and 2023, but the absolute number is undisclosed and clearly still very small. Bekaert projects a market worth €500m by 2030.

In 2023 Bekaert announced a collaboration with Toshiba to move downstream to make the whole membrane-electrode assembly (MEA), which comprises the PTL as well as anode and cathode catalyst layers, membrane and carbon gas diffusion layer. The two firms plan to use Toshiba’s breakthrough technology to reduce iridium requirement by 90%, which would be a key USP given iridium’s high cost. The suggested possible market size is €2-4bn.

I am not thrilled with Bekaert’s early-stage and currently unprofitable focus on green hydrogen products. But I am reassured that the total amount they will invest should be modest, at least until they get tangible signs of commercial momentum. In the meantime, management’s overall commitment to the group profitability targets should mean that the costs of the hydrogen push are kept small.

Other specialty products are hose reinforcement, burners and heat exchangers, and the remaining solar and semiconductor ingot cutting wires. These businesses are not too special, and will be managed for margin.

Bridon-Bekaert Ropes Group (14% of sales, 16% of EBIT)

This is a satisfying story of how Bekaert gained a substantial business essentially “for free”.

Bridon is a UK steel ropes business that was separately listed from 1978 until 1997, when it was acquired by FKI for £130m. FKI in turn was bought by Melrose, the listed turnaround specialists, in 2008. In 2014, Melrose sold Bridon to Ontario Teachers Pension Plan for £365m, based on 2013 sales of £266m and OP of £42m.

Sadly for OTPP, Bridon’s key markets of oil and gas and mining collapsed right after the acquisition. They looked for a face-saving exit, and Bekaert was happy to help.

In mid 2016, Bekaert agreed to merge Bridon with their own steel rope business. This was a clever joint venture for Bekaert, who gained 67% share in the combined business, despite Bridon being the bigger business. The deal was struck on a cash-neutral basis, with the JV taking on €279m of ring-fenced debt from Bridon. The combined business was called Bridon-Bekaert Ropes Group, or BBRG.

OTPP’s share of losses from BBRG was €14m in 2016 and €21m in 2017. The outlook for 2018 was even worse. These were not just accounting losses either – further cash injections would be required.

OTPP did not have the stomach for this. It effectively chose to hand the keys to Bekaert and walk away.

In April 2018, OTPP completed its exit by selling its minority stake to Bekaert for just €7.7m, plus repayment of a €61m shareholder loan.

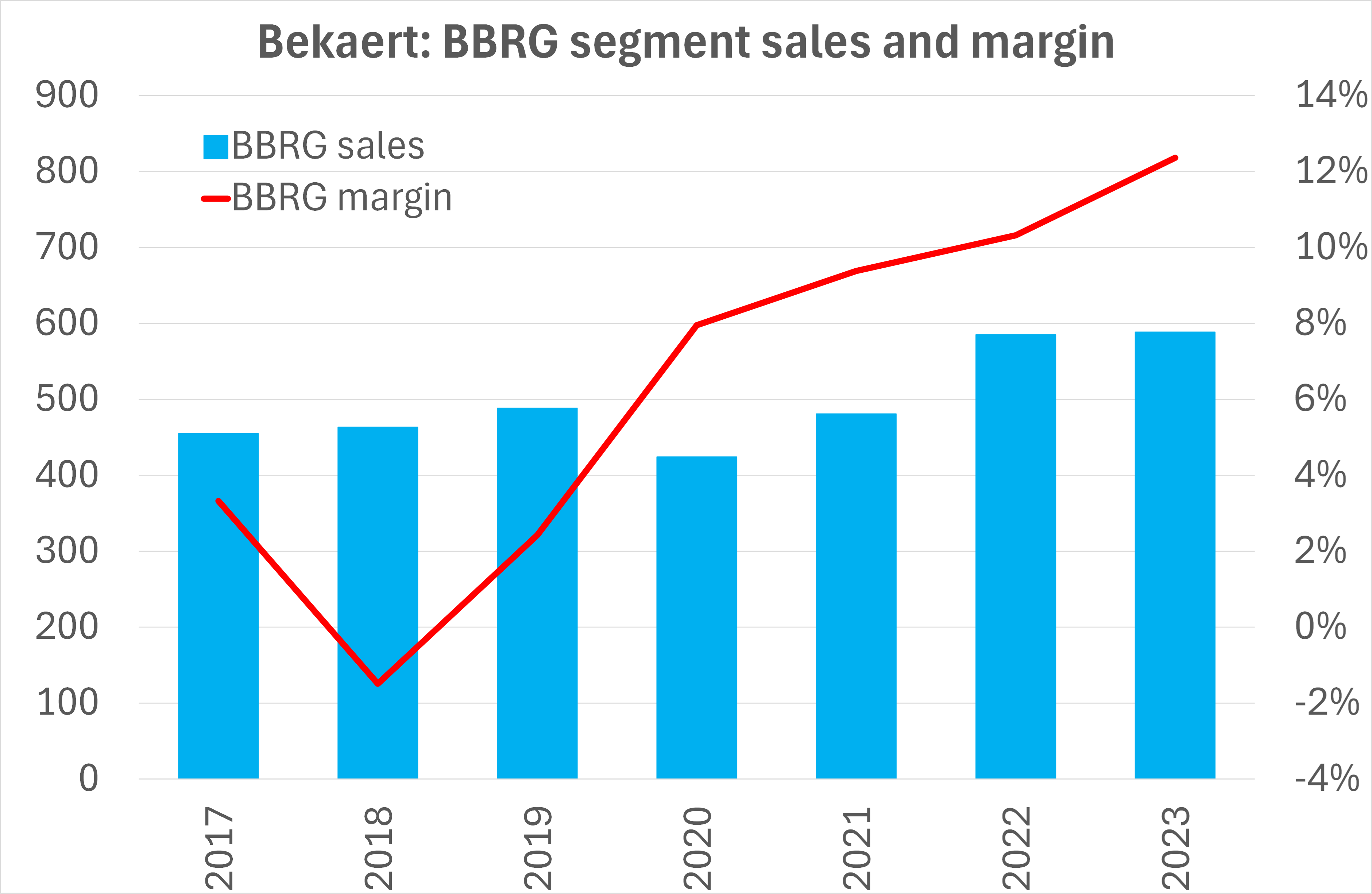

Once Bekaert had 100% control of BBRG, and especially with the arrival of the new chairman and management team in 2019, a miraculous recovery took place. See chart below.

Of course the margin recovery was not so miraculous. They stepped away from low-margin business, closed two loss-making plants in Canada and Germany, and raised prices and cut costs on the rest of the book of business.

Today BBRG is an attractive, well-run business. It has a global footprint and serves mining, energy, crane, elevator, fishing and other markets.

The best growth prospect for BBRG is in innovative floating offshore wind mooring solutions, as well as offshore lifting ropes and slings. BBRG is the world leader, having conducted projects with Equinor, BW Ideol and Stiesdal.

In oil and gas, Bekaert offers an Armofor tape product to reinforce non-metallic pipe, serving Aramco and ADNOC who see significant lifecycle cost savings and a reduced environmental footprint from steel-reinforced thermoplastic pipes (SRTP) compared to steel pipes. The go-to-market is a supply agreement with the plastic pipe makers, who have chosen Armofor.

Bekaert projects double-digit growth for BBRG out to 2026, thanks to these growth platforms.

BBRG’s key competitors include an impressive listed Indian company and a less impressive US business owned by private equity.

Usha Martin (USHAMART.NS, $1.3bn market cap) is a listed Indian competitor in wire rope. It divested its steel-making operation in 2019, which improved its balance sheet, profitability and return on capital.

Usha has 45% of sales in India and 55% in overseas markets, including 24% Europe, 15% Asia Pacific, 9% Middle East & Africa and 7% America. Usha’s EBITDA margin reached 18.6% in FY24, ahead of BBRG’s 16.8% in 2023.

WireCo is the key US-based competitor to Bridon. It was acquired by Paine private equity in 2007. It struggled with high debt and interest costs. In 2016 Onex private equity acquired majority control in a transaction that reduced debt somewhat. By the end of 2022, WireCo was reportedly in improved financial health and investing $25m into one of its Missouri facilities for crane rope. However, S&P continues to rate it ‘B’, two notches into junk, reflecting still-high leverage and vulnerability to higher interest rates.

Tokyo Rope (5981.T, $135m market cap) is listed in Japan, with poor profitability.

History

Bekaert was founded as a barbed wire fencing maker in 1880 in a village outside Kortrijk, in West Flanders. Leo Leander Bekaert patented a better design for barbed wire, using star-shaped crowns with six sharp points.

Bekaert has remained mainly focused on wire products ever since. Steel tyre cord followed in the 1950s, as Bekaert facilitated the important tyre industry switch from bias to radial tyres.

The company went global, opening bases in north and south America and Japan during the 1950s. Bekaert has been a true multinational for a long time.

The IPO was in 1972, to raise funds for further international expansion. However, the aristocratic Bekaert family kept a controlling stake, which it has maintained until this day. More on that below.

By 1990 Bekaert reached 15,000 employees. The business stagnated for the next 15 years, until China started booming from 2005 to 2010. Both tyre cord and especially solar ingot sawing wire contributed to bubble conditions for Bekaert in 2010. Net profit hit a record €368m and the market cap briefly touched over €5bn.

This boom was over in a flash, as Chinese companies quickly learnt to copy the diamond sawing wire product. The experience destabilised Bekaert, which remained in a funk for the next seven years or so under an ineffective board and management.

Throughout the 2010s there were attempts at portfolio changes, restructuring and profit improvement. But these proved inadequate to the prevailing tough conditions. Profits bounced along at a low level. High working capital ensured low free cash flow and poor returns on capital.

Despite a false dawn with a better 2016 and 2017, the year 2018 saw Bekaert once again sink close to rock bottom. The profit margin fell below 5% even on an adjusted basis. Net debt was uncomfortably high at around 3x EBITDA, and free cash flow was low.

Management changes

In 2019, the board opted for change by bringing in Jürgen Tinggren as new chairman, effective from May 2019.

(The outgoing chairman, Bert De Graeve, had been elevated from CEO to chairman in 2014. He had served as CEO from 2006 to 2014, and before that as CFO from 2002 to 2006. His 17 years in top leadership positions at Bekaert had delivered mediocre results at best.)

Tinggren, a Swedish national, was a top calibre appointment, having been CEO of global elevator firm Schindler from 2007 to 2017. He previously worked at Sika for 12 years, another excellent business.

Tinggren quickly recruited a new CFO, Taoufiq Boussaid, in July 2019. Boussaid was a seasoned global executive from Bombardier, United Technologies / Carrier, and Coca-Cola Company. He had operational as well as finance experience. Boussaid remains in post today.

Tinggren brought in his former Schindler colleague, Oswald Schmid, as COO in December 2019. Schmid had worked in Schindler since 2002, and served on the group executive committee since 2013.

Four months after Schmid joined Bekaert, in March 2020, CEO Matthew Taylor stood down “for personal reasons” and Oswald Schmid became Bekaert’s CEO, at first on an interim basis. From March 2021 the appointment was made permanent.

Schmid retired in August 2023. He was replaced as CEO by Yves Kerstens, who had joined Bekaert in April 2021 as divisional CEO of Specialty and as COO. A Belgian national, Kerstens came from Axalta Coating Systems and Bridgestone.

The board itself has also undergone renewal and shrinkage. It is now down to nine directors – hardly streamlined, but far better than the 15 members in 2018.

Family shareholding

The Bekaert family are literally Belgian aristocracy. (They are not alone – 20 of the largest companies on the Brussels stock exchange are owned by seven noble shareholders, according to this fascinating article on the enduring financial success of the Belgian aristocratic families.)

The Bekaert family continues to own a 36.4% controlling stake as of Dec’23. Despite there now being apparently 200 or more family owners, the stake is maintained in a holding company and concert party structure, which to date has served to maintain control.

The family-controlled board finally approved the switch a radical new chairman and management team in 2019. In my view, this derisks any danger of malign or incompetent influence they might have on the business.

We can presume that the family interests are basically aligned with minorities in wanting high profits and dividends, plus a sound financial structure with low risk of dilution.

The large buyback programme that took place in 2022 to 2023 was supported by the family, who committed to sell shares pro rata into the buyback in order to leave their stake unchanged at 36%.

Financial review

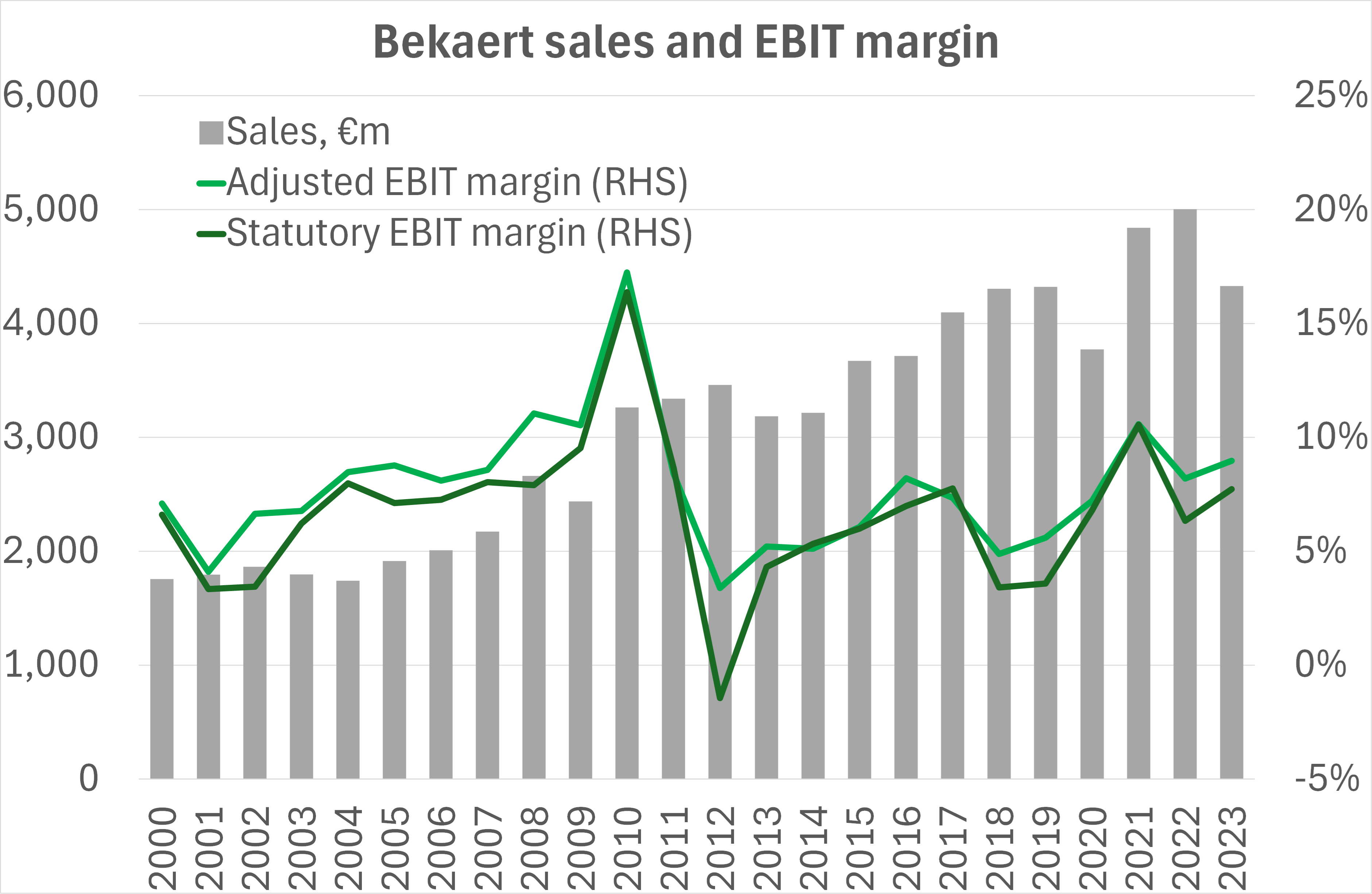

As discussed above, Bekaert’s long-term track record is not especially impressive. My chart below shows a 4% sales CAGR from 2000 to 2023, with a similar growth rate for EBIT and EPS. While this is better than many other European industrials, I prefer to compare it to the universe of high quality stocks I can own in any sector.

Note that the margin, though often low, was rather stable throughout the period – with absolutely no losses on an adjusted basis, for example.

This reflects the pass-through nature of Bekaert’s model. The price of the key inputs, wire rod and energy, fluctuate significantly over time. However, Bekaert has robust pass-through mechanisms in place to adjust prices in a timely fashion.

Bekaert’s habit of taking frequent exceptional costs and impairments can also be seen, with the gap between adjusted and statutory margin. This is not a problem: I simply forecast for restructuring costs to continue. I base my valuation and my quality assessment entirely on the statutory results and cash flows. Consensus also allow for ongoing exceptional costs.

The anaemic long-term growth rate translated into sub-par returns for the stock. My chart below shows that by the end of 2018, Bekaert had underperformed both the S&P500 and also the weaker MSCI EAFE index. This underscored the need for management change.

Bekaert’s ROCE track record is shown below. The post sawing wire slump is clearly visible, with an eight-year period in which the company was clearly failing to earn its cost of capital. Under new management, ROCE has been at a satisfactory mid-teens rate, despite some tough cyclical conditions.

Underlying this, the new management team has taken decisive steps to reduce headcount. The chart below shows EBIT per employee in each of the last three years has exceeded the previous peak, aside from the solar sawing wire bubble year.

As we saw at the top, free cash flow has improved dramatically under new management. This is especially thanks to much better working capital control.

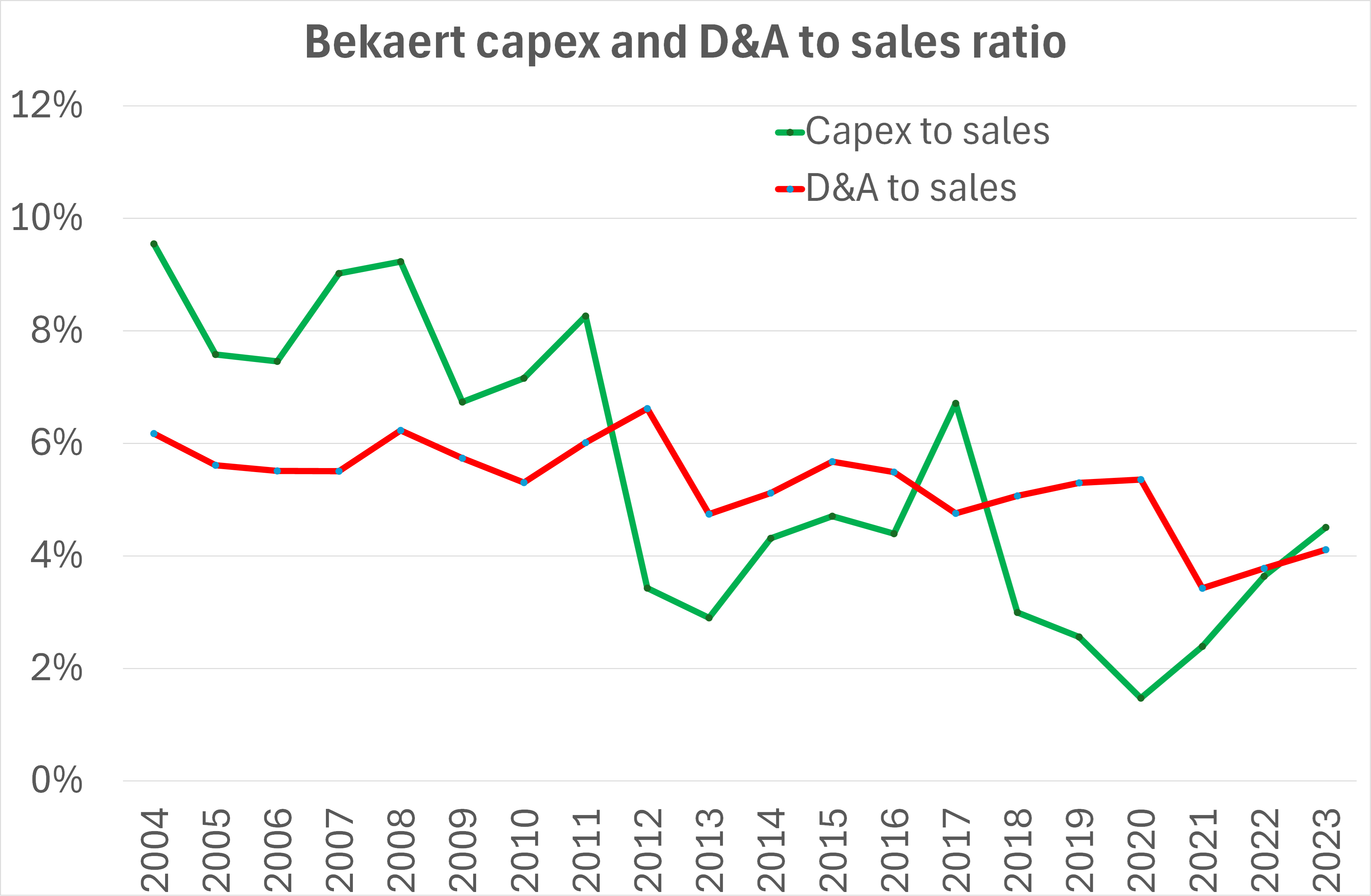

Bekaert invested heavily in growth in the first decade of the century. But since 2012, it has enjoyed a low capex to sales ratio of around 4%. This reflects the less capital intensive nature of its processing activity, compared to primary steelmakers and many other manufacturers. See chart below.

Thanks to the strong free cash flow and improved profitability, and even after funding a €230m buyback, Bekaert’s stated leverage is lower than at any time this century.

I note that Bekaert uses factoring, to the tune of €232m in 2023. In addition, Bekaert operates a reverse factoring agreement to the tune of €51m. This allows suppliers to receive early payment from a bank at a discount.

I am not a fan of either programme. I add back the €283m to my adjusted net debt figure, to reflect the additional debt that Bekaert would need to borrow if forced to unwind these arrangements.

Happily, it’s a moot point in this case, because Bekaert’s gearing remains very low at c.1x net debt to EBITDA even after adjusting for the supply chain finance.

Bekaert’s borrowing costs are very low, at 3.06% blended in 2023, thanks to fixed rate bonds and Schuldschein loans issued at favourable low rates. We can expect Bekaert’s blended rate to tick up in the medium term as the cheap debt matures, but interest expense should stay low in absolute terms thanks to the low debt burden.

Bekaert has a number of non-consolidated JVs and associates, as well as some consolidated businesses with minority partners. The chart below shows the signficant positive contribution from JVs and associates. Two 45%-owned Brazilian JVs are the biggest contributors, spanning the range of Steel Wire Solution and tyre cord activities. Since the sale of the Chile and Peru business, there are no minorities left in any business of size.

Estimates and valuation

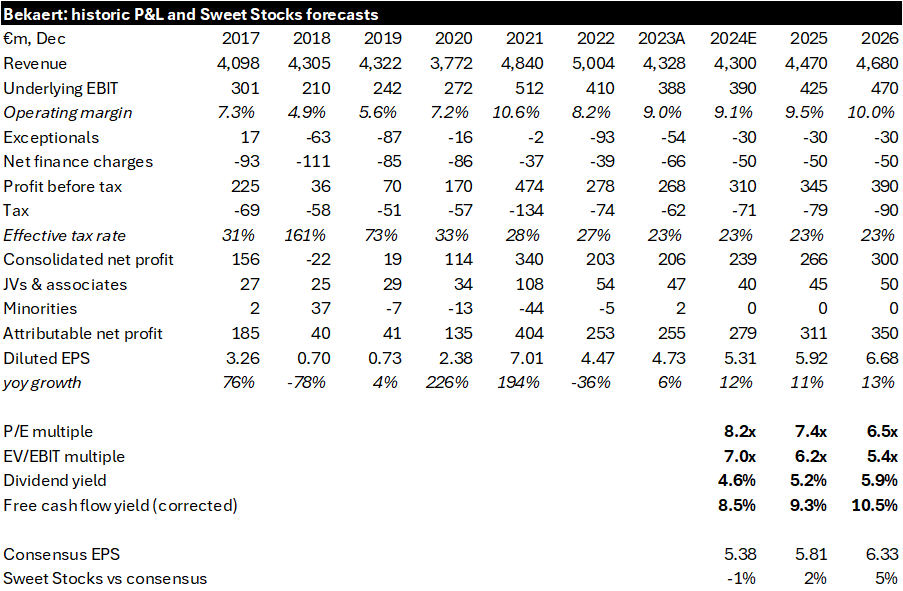

Bekaert earnings peaked in 2021, on a favourable combination of 9% volume growth from post-lockdown restocking and a 13.5% move up in wire rod prices. The EBIT margin reached the exceptional level of 10.6%.

2022 saw another big 21% price jump amid the global inflationary environment, but this time offset by a 9% fall in volumes. The margin fell back to a still-respectable 8.2%.

2023 saw a -9% reversal of inflation as well as a further 4% fall in volumes amid recessionary conditions in several countries and sectors. Bekaert delivered an improved 9.0% margin which was impressive in the circumstances.

Given this recent volatility, it’s good to see that Bekaert’s consensus estimates have been fairly stable over the last year or longer. Analysts expect EPS of €5.38 in 2024 and €5.81 in 2025 – much the same as 12 months ago.

For its part, management has guided to “modest sales growth and at least stable margins” in 2024E, followed by the mid-term guidance of 5% average sales growth and a 10% EBIT margin by 2026.

I find Bekaert’s guidance credible, and I strike my estimates in accordance. This also leaves me pretty close to consensus. See my table of estimates and valuation metrics below.

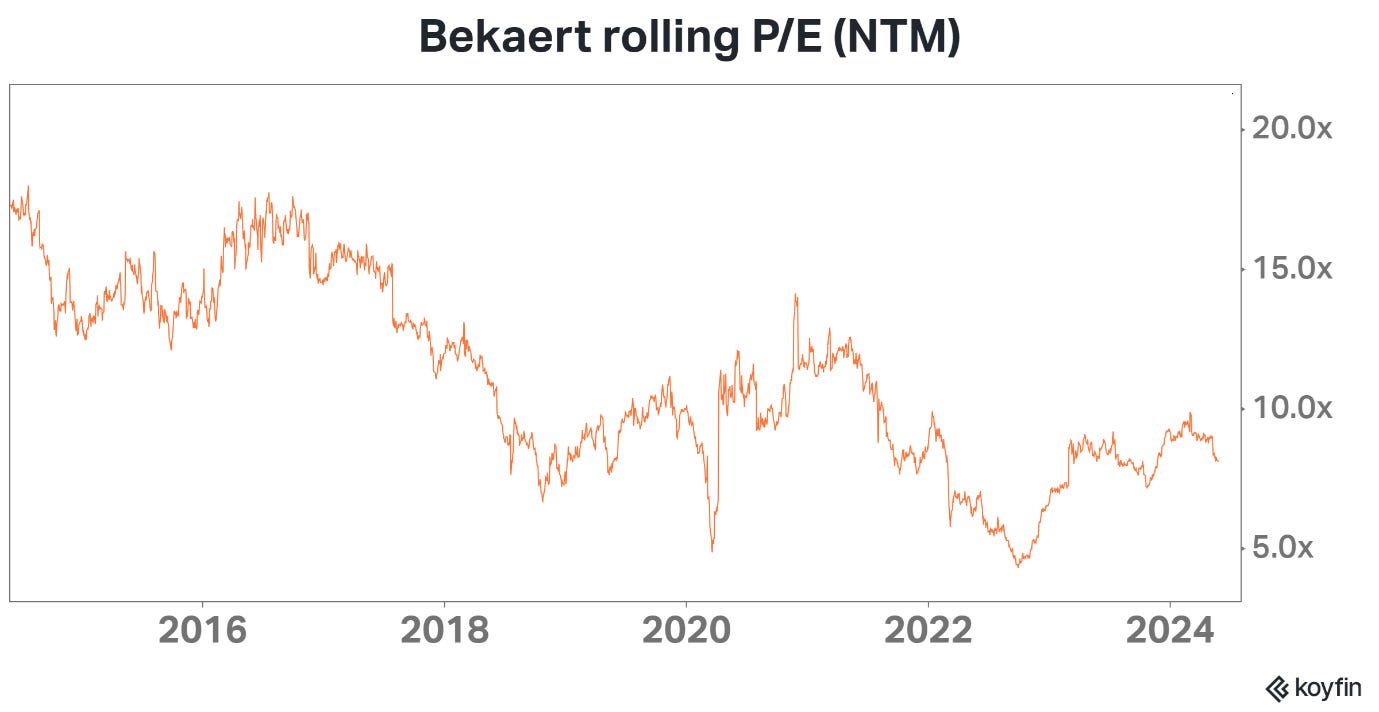

It is immediately clear that Bekaert is extremely cheap. It trades on 8x P/E or 8.5% FCF yield.

The chart below shows that Bekaert has de-rated in the last 2-3 years.

Why so cheap?

· The long-term track record is admittedly mediocre. Some may be suspicious that Bekaert’s recent higher margins are fluky or temporary, rather than the sustainable product of an impressive turnaround by a skilled new management team.

· Bekaert sits in a low quality sector (Materials / Metals & Mining). Many quality-focused investors shun the sector entirely.

· The stock is highly illiquid for institutional fund managers, trading less than $2m per day on average.

· The dividend payout ratio is below 40%, and the excellent buyback was suspended in early 2024. This was to allow for greater reinvestment into the business, in the form of bolt-on M&As and possible higher capex towards hydrogen electrolysis components. Investors may be dubious that this investment will create value, compared to the alternative of full cash returns to shareholders.

While these objections have some merit, the stock will be forced to work if it delivers earnings in line with guidance and consensus. My assessment of management is positive, and I regard their guidance as conservative and achievable.

Hill & Smith in the UK (HILS.L, $2.1bn) is a rare example of a company in the Metals sector with high returns, good growth and a strong reputation for capital allocation. It trades at 18x forward P/E, double the Bekaert multiple. While Bekaert certainly doesn’t deserve to trade at 18x today, the HILS example does show that it would be reasonable for Bekaert to re-rate upwards over time if it keeps building its track record.

I’ve therefore started a position in Bekaert, which I intend to build over the coming months.

CORRECTION 10:30 on 27/05/2024

NB this post has been corrected at 10:30am on 27/05/2024 for the free cash flow calculation.

The initial draft of the post gave a wrong figure of €1.5bn for cumulative FCF from 2019 to 2023 inclusive, having failed to correct for lease payments in the footnotes to the financing section of the cash flow statement.

The reconciliation and correction is shown in the table below.

Many thanks to @GPK992 on Twitter for the spot.

Thanks for the write-up! Even as a Belgian, I never looked in depth at Bekaert. Here's an overview of my (lazy) perception from occasionally briefly glancing at the company:

- Before new management: cyclical debt-laden european industrial (stay away!)

- New mgmt: ok, has potential, but need to see results

- 2021: temporarily inflated profits, "don't buy on cyclical peak of earnings!"

- red flags in quick CEO turnover

- 2023-now: insider share sales

I assume i'm not the only one who looked at the stock like this.

Thanks for highlighting the company. Seems like it has more potential than I thought

Very in depth analysis Alex . Interesting to hear what happened to Bridon after Melrose sold it . Thanks for your efforts .